Table of Contents

- 1. Growth opportunities for ISPs in Mexico

- 2. Growth of the ISP market in Mexico

- 3. Dominance of the main fixed broadband providers

- 4. Opportunities for WISPs in underserved areas

- 5. Importance of investment in fiber optics

- 6. Maximizing bandwidth with advanced technologies

- 7. Adoption of artificial intelligence in network management

- 8. Service diversification to attract customers

- 9. Strengthening customer support

- 10. Collaboration with industry players

- 11. Strategies for the Future of ISPs in Mexico

Growth opportunities for ISPs in Mexico

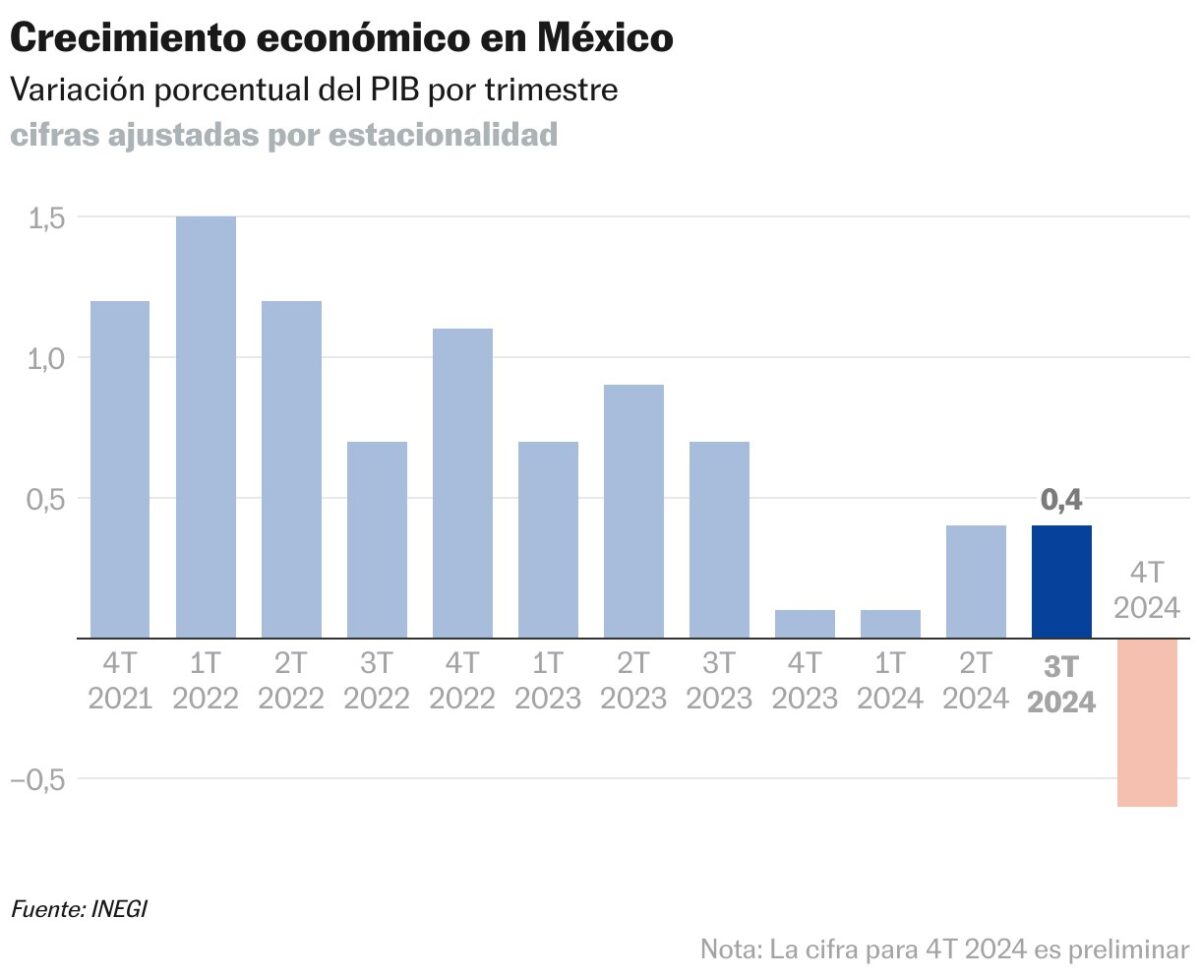

The Mexican internet market continues to expand, driven by demand for higher speed, stability, and coverage. In broadband, reported annual growth is around 9.1% in fixed and ~23.6% in mobile, a sign of sustained appetite for connectivity and an increasingly data-intensive user. At the same time, penetration still below international benchmarks creates room for new deployments, especially outside the most competitive urban corridors.

For an ISP—and particularly for regional operators and WISPs—the growth path combines three fronts: infrastructure (fiber and transport), operational efficiency (automation and AI), and commercial differentiation (services and support).

Priorities to Scale the ISP

– Infrastructure (capacity and coverage): decides where to grow (areas) and on what foundation (backhaul, fiber, redundancy where applicable).

– Operational efficiency (cost per customer): decides how to operate at scale (automation, NOC, support processes, clean data).

– Commercial differentiation (ARPU and churn): decides why they choose you (installation/support, bundles, services for SMEs, security).

Practical point: if today your main pain is saturation/complaints, start with infrastructure and operations; if your network is stable but growth stalls, prioritize differentiation and channels.

Growth of the ISP market in Mexico

Mexico is undergoing a transition: more households and businesses depend on the internet for work, education, entertainment, and cloud services. That shift raises the minimum standard: it’s no longer enough to “have coverage”; the customer demands low latency, continuity, and fast support.

The opportunity lies in two layers:

- Geographic expansion: semi-urban and rural localities where demand exists, but supply is limited or low quality.

- Quality improvement: migration from saturated networks or those based on legacy technologies to fiber and scalable transport, to sustain traffic growth.

| Growth axis | Fixed broadband (home/SME) | Mobile broadband (complement/competition) | What it means for a regional ISP/WISP |

|---|---|---|---|

| Geographic expansion | High opportunity in areas without FTTH or with poor experience | Can “cover” quickly, but does not always replace stability/unlimited plans | Focus on localities where mobile doesn’t solve it (capacity, stability, cost per GB) |

| Quality improvement | Migrating to fiber and better transport reduces congestion and complaints | Improvement depends on the mobile operator’s spectrum/cells | Differentiate through consistency (latency/stability) and support |

| Market signal (estimates) | Reported annual growth ~9.1% | Reported annual growth ~23.6% | Use it as a thermometer, not a promise: it varies by source, cutoff, and methodology (e.g., MDC Data Centers) |

Dominance of the main fixed broadband providers

Fixed broadband is highly concentrated. Industry reports indicate that Telmex-Telnor, Televisa, and Megacable account for more than 90% of the fixed segment (depending on the cutoff and the report source). That reality imposes barriers: economies of scale, already-depreciated infrastructure, and brands with high recall.

But concentration also leaves gaps: areas where the big players don’t prioritize investment, long installation times, or customer service perceived as poor. There, a regional ISP can compete with a clear proposition: fast installation, consistent service, and close support.

Competing with incumbents: advantages and risks

Typical barriers when you compete against incumbents

– Scale and costs: they can sustain aggressive pricing in key areas.

– Existing infrastructure: backbone and last mile already deployed.

– Brand and channels: greater recall and commercial presence.

Exploitable gaps (where a regional player usually wins)

– Non-priority areas: neighborhoods/peripheries/localities where investment is deferred.

– Installation time: clear promise and delivery (scheduling, inventory, crews).

– Support and resolution: proximity, proactive communication, and lower MTTR.

Trade-off to watch: growing “on price” accelerates sign-ups, but can trigger congestion and churn if backhaul doesn’t grow at the same pace.

Opportunities for WISPs in underserved areas

WISPs tend to grow where fiber is slow to arrive or where the return on investment is slower for national operators. In underserved areas, the competitive advantage is agility: faster deployments, knowledge of the terrain, and the ability to tailor packages to the local economy.

Keys to capturing it:

- Design coverage based on real demand: prioritize communities with schools, businesses, and microenterprises that require stable connectivity.

- “Primero quality, then scale”: avoid early overselling; reputation in small towns is built or lost in weeks.

- Robust backhaul: the bottleneck is not the wireless last mile, but transport; without good backhaul, growth turns into complaints.

Operational Readiness to Grow

– [ ] Validate demand with concrete signals: schools/remote work, businesses with digital payments, internet cafés, recurring complaints about the current provider.

– [ ] Define a “minimum quality” before selling: real speed at peak hours, target latency, and oversubscription policy.

– [ ] Secure backhaul before expanding cells: contracted capacity, redundancy where feasible, and saturation monitoring.

– [ ] Standardize installation: CPE checklist, alignment, throughput/latency tests, and parameter logging.

– [ ] Power and weather plan: UPS/batteries where it hurts, grounding, and a storm protocol.

Importance of investment in fiber optics

Fiber optics has become the technological “floor” for competing on capacity and stability. Even when the last mile is wireless, fiber in the core and in trunks makes it possible to:

- Scale capacity without redesigning the entire network.

- Reduce failures associated with saturated links.

- Improve experience in sensitive applications (video calls, gaming, cloud).

In the Mexican ecosystem, technology providers have pushed the idea that WISPs evolve into operators with a greater fiber component, relying on partnerships and deployment models that reduce initial CAPEX.

Fiber to scale with stability

– Market signal: the reported growth of fixed and mobile broadband (e.g., figures shared by MDC Data Centers) is usually accompanied by more consumption of video, cloud, and remote work; that puts pressure on sustained capacity and stability, where fiber tends to perform better.

– Operational evidence (what changes in the field): when moving trunks/backhaul to fiber, you typically see less degradation at peak hours, fewer “micro-outages” due to interference (vs. long wireless links), and a better margin to grow without constant re-engineering.

– How to reduce CAPEX/time: partnership models with InfraCo can speed up deployment and lower initial investment (example approach: Internexa).

– Evolution path for WISPs: there are providers that are driving the transition toward more fiber and the use of optical technologies to scale (e.g., DPL News coverage of Padte initiatives

c with WISPs in Mexico).

Maximizing bandwidth with advanced technologies

When traffic grows, the challenge is not just “more megabits,” but transporting them efficiently. Optical technologies and automation make it possible to increase capacity without multiplying operating costs at the same pace.

Use of DWDM

DWDM (Dense Wavelength Division Multiplexing) makes it possible to multiply the capacity of a fiber by carrying multiple wavelengths on the same strand. In practical terms, it helps to:

- Increase backbone capacity without laying new fiber.

- Optimize routes between nodes and exchange points.

- Prepare the network for growth in enterprise customers and higher residential consumption.

For regional ISPs, DWDM can be the step that turns a “functional” network into a scalable network, especially when the cost or complexity of civil works limits new routes.

Benefits of automation

Automation reduces response times and human errors in repetitive tasks:

- Faster provisioning (new sign-ups, plan changes, activations).

- Monitoring and alerting with thresholds and event correlation.

- Capacity management based on data, not intuition.

The result is usually twofold: fewer outages and lower cost per customer served, two critical variables for scaling without losing margin.

| Lever | What problem it solves | Typical impact on operations | When to apply it first |

|---|---|---|---|

| DWDM | Lack of capacity on trunks/backbone without a quick possibility of laying new fiber | More capacity per fiber; better transport scalability (referenced in sector discussions such as DPL News/Padtec) | When the bottleneck is transport and civil works are slow/expensive |

| Automation (provisioning/monitoring) | Slow sign-ups and changes; manual errors; reactive NOC | Fewer configuration-related failures; faster response; more consistent operations | When the pain is operational (tickets, times, errors) and you already have basic telemetry |

Adoption of artificial intelligence in network management

AI is moving from a “trend” to an operational tool. In ISP networks, its value shows up in three concrete uses:

- Predictive maintenance: detect patterns that anticipate ofgradation (noise, micro-outages, saturation).

- Performance optimization: dynamic prioritization, congestion analysis, and expansion recommendations.

- Assisted customer support: ticket classification, diagnostic suggestions, and reduced mean time to resolution.

In a market where users compare experiences, AI does not replace the technical team: it makes it faster and more consistent. In practice, this usually translates into pre-classification by contact reason, SLA-based prioritization, retrieval of customer context, and escalation to a human when the case requires it, maintaining conversation traceability.

Gradual implementation of telecom AI

1) Choose 1–2 use cases with clear pain (e.g., saturation prediction or ticket classification). If there is no measurable pain, AI becomes a “demo”.

2) Ensure minimum data: network inventory, telemetry/alerts, ticket history, and fault catalog. Without this, the model learns “noise”.

3) Scoped pilot (4–8 weeks): define metrics before running (MTTR, recurrence, % of tickets correctly classified, false positives).

4) Integrate into the real workflow: NOC/support must be able to accept/reject recommendations and leave traceability.

5) Quality checkpoints: review weekly for biases (areas/equipment), model degradation, and network changes.

6) Scale by modules: support/NOC first, then capacity optimization; avoid “big bang”.

Trend reference: analysis of AI/automation in telecom toward 2030 (Aipix).

Service diversification to attract customers

“Internet only” tends to become commoditized. To grow, many ISPs expand their offering with higher-value services:

- Packages (bundles): internet + voice + TV/OTT, where applicable.

- Business services: dedicated links, PBX/IP telephony, managed Wi‑Fi, backup and continuity.

- Video surveillance as a service (VSaaS) and security solutions for shops and residential developments.

- Cloud and storage: from basic backups to managed services.

Diversification increases revenue per customer and reduces churn: when the ISP solves more needs, switching providers becomes more costly for the user.

| Service (examples) | Natural segment | Main value | When it is usually a good first bet |

|---|---|---|---|

| Managed Wi‑Fi | Premium home / SMB | Fewer “it’s the Wi‑Fi” complaints; better experience | If your support team receives many internal Wi‑Fi tickets |

| PBX / IP Telephony | SME | Differentiation and higher ARPU | If you already have business customers and can provide basic support |

| VSaaS (video surveillance) | Retail / gated communities | Recurring revenue and a “stickiness” anchor | If you have installers and can monitor/manage (trend cited by Aipix) |

| Backup/continuity (failover) | SME | Reduces the customer’s operational risk; lowers churn | If your network is stable and you can offer SLA/support |

| Bundles (voice/OTT) | Residential | Retention and perceived value | If you have agreements/partners and billing ready |

Strengthening customer support

In regional ISPs, support can be the main differentiator. The recipe is not “more call center,” but processes:

- Structured diagnosis for typical failures (CPE, internal Wi‑Fi, congestion, power outages, backhaul).

- Proactive communication during incidents: estimated times, progress, and closure.

- Operational metrics: mean response time, mean time to repair, recurrence by area/equipment.

Solid support turns inevitable problems (weather, power outages, public works) into a manageable experience for the customer.

Operations and Support with KPIs

– [ ] FRT (first response time) defined by channel (WhatsApp/phone/ticket) and measured by shift.

– [ ] MTTR (mean time to repair) by failure type (CPE, last mile, backhaul, power).

– [ ] Recurrence / recontact by area and by equipment model (to tackle root causes).

– [ ] Layered diagnostic script: customer (power/Wi‑Fi) → CPE → access → transport → core.

– [ ] Communication templates for incidents (start, update, closure) with a realistic ETA.

– [ ] Living knowledge base: each major incident leaves “what happened / how it was detected / how it is prevented”.

Practical reference: troubleshooting approaches for ISPs (Ozmap).

Operational signals worth measuring from the start

For support to scale without losing quality, it’s advisable to standardize and periodically review: first response time, mean time to repair, and recontact/recurrence rate by area, cause, and equipment type.

Collaboration with industry players

Growing faster often requires allizas:

- InfraCo and carriers for transport and accelerated deployment.

- Technology providers for modernization (optical, DWDM, automation).

- Connectivity programs and initiatives to expand coverage in underserved areas.

- Industry events and networks (for example, industry meetups) to close deals and learn best practices.

Collaboration reduces CAPEX, shortens timelines, and makes it possible to compete with larger operators.

Ecosystem of strategic partners

– InfraCo (infrastructure): goal = accelerate deployment and lower CAPEX; useful when civil works are the bottleneck (reference: Internexa).

– Carriers / transport: goal = robust and scalable backhaul; key to preventing growth from turning into saturation.

– Vendors / integrators: goal = operational modernization (optical, DWDM, automation) and knowledge transfer.

– Connectivity programs and initiatives: goal = expand coverage where there is a gap; they usually require orderly execution and reporting.

– Industry events: goal = networking and benchmarking; for example, EXPO ISP MX-type spaces (mentioned in SOCIUM).

Strategies for the Future of ISPs in Mexico

The future of the Mexican ISP will be defined by whoever manages to combine expansion with quality, and technology with customer closeness.

Key trends 2024–2030

Trends that most often move the needle (2024–2030, according to industry discussions):

– Smarter operations: automation and AI for NOC/support and predictive maintenance (Aipix).

– More “enterprise-like” services: security, VSaaS, managed Wi‑Fi, and specialized connectivity.

– Internet that is more “secure by default”: adoption of IPv6 where appropriate and practices like secure DNS (mentioned in SOCIUM).

– Connectivity for businesses: private networks (including the conversation about private 5G in the IT/telecom channel; e.g., InfoChannel) for specific use cases.

– Talent and documentation: standardize operations so growth doesn’t depend on heroes.

Importance of Continuous Innovation

Demand does not stabilize: it grows and changes. Innovating means upgrading transport, improving monitoring, adopting IPv6 where appropriate, and modernizing operations to sustain new uses (cloud, video, IoT).

Adapting to Customer Needs

Households ask for stability; businesses ask for

n SLA and response. Segmenting plans by usage profile, and not only by “megabits,” helps sell better and operate with less friction.

Sustainability and Social Responsibility

Expansion into underserved areas has a direct impact on education, productivity, and access to services. Integrating energy efficiency, preventive maintenance, and responsible deployments improves costs and reputation.

Strengthening Cybersecurity

The larger the customer base, the larger the attack surface. Security must grow with the network: secure DNS, mitigation of common threats, good configuration practices, and continuous monitoring.

Development of Human Talent in the Sector

The shortage of technical profiles can slow growth. Training field crews, the NOC, and support—and documenting operations—is as strategic as buying equipment.

How to Grow an ISP in Mexico

Understanding the ISP Market in Mexico

The market is growing, but it is concentrated. The real opportunity lies in quality, speed of execution, and smart coverage in areas the big players don’t prioritize.

Key Strategies for ISP Growth

- Expand where there is unmet demand.

- Raise quality with fiber and scalable transport.

- Operate efficiently through automation and AI.

- Differentiate with services and support.

Infrastructure Development

Investing in fiber (your own or through partnerships), strengthening backhaul, and designing redundancies where the business justifies it is the foundation for growing without collapsing due to saturation.

Adoption of Emerging Technologies

DWDM, automation, and AI make it possible to scale capacity and operations. They also open the door to more sophisticated offerings for businesses and local governments.

Diversification of the Service Offering

Bundles, managed services, VSaaS, and solutions for SMEs increase revenue per customer and reduce churn.

Strengthening Customer Support

Processes, metrics, and proactive communication turn support into a competitive advantage, especially in regional markets.

Leveraging Marketing and the Brand

A clear brand—“we install fast,” “local support,” “stable internet”—works better than generic speed promises. Reputation in communities is built through follow-through.

Collaboration with industry stakeholders

Partnerships with carriers, InfraCo, providers, and connectivity programs accelerate deployments and reduce the cost of entering new areas.

Challenges and opportunities

The challenge is competing against scale and dominant brands; the opportunity is to capture niches with superior execution, the right technology, and closeness to the customer.

Sustainable growth process

1) Diagnosis (2–4 weeks): network map (capacity/backhaul), tickets by cause, areas with churn, costs per installation and per support.

2) Growth thesis: choose 1 priority (geographic expansion or quality improvement) and 1 differentiator (support/installation/services).

3) Network plan: define transport upgrades (fiber/DWDM where applicable), redundancies “where it hurts,” and installation standards.

4) Operational plan: automate what’s repeatable (provisioning/monitoring), define metrics (FRT/MTTR/recurrence), and a knowledge base.

5) Go-to-market: packages by profile (home/SMB), a clear value proposition, and a billing/retention process.

6) Monthly improvement cycle: review saturation, complaints, installation times, churn, and margin; adjust capacity and processes before opening new areas.

Key checkpoint: if sign-ups rise but peak-hour complaints also rise, stop expansion and fix transport/capacity.

Conclusion

Growing an ISP in Mexico requires a comprehensive strategy: invest in infrastructure (especially fiber and transport), maximize capacity with technologies like DWDM, operate with automation and AI, diversify services, and turn support into a differentiator. In a concentrated market that still has coverage and quality gaps, agile operators—especially WISPs and regional providers—can gain ground where connectivity is still a promise yet to be fulfilled.

This implies not only investing in fiber, DWDM, and backhaul, but also operating efficiently and turning support into a real differentiator. From Suricata Cx’s perspective, automation and AI applied to telecom workflows (with human control) help reduce response times and cost per interaction, and sustain quality as the subscriber base accelerates.

This approach prioritizes hybrid models (automation + human oversight) and integration with real ISP/telecom operations to scale support, sales, and collections without fragmenting channels.

Martin Weidemann is a specialist in digital transformation, telecommunications, and customer experience, with more than 20 years leading technology projects in fintech, ISPs, and digital services across Latin America and the U.S. He has been a founder and advisor to startups, works actively with internet operators and technology companies, and writes from practical experience, not theory. At Suricata he shares clear analysis, real cases, and field learnings on how to scale operations, improve support, and make better technology decisions.