Table of Contents

- 1. Launch of CaixaBank’s AI agent

- 2. Functions of the AI agent in the application

- 3. Interaction between the AI agent and human specialists

- 4. Current use of the agent in loan applications

- 5. Technology behind the AI agent

- 6. Conclusions on the implementation of CaixaBank’s AI agent

- 7. Suricata Cx: Transforming the Customer Experience in Telecommunications

Launch of CaixaBank’s AI agent

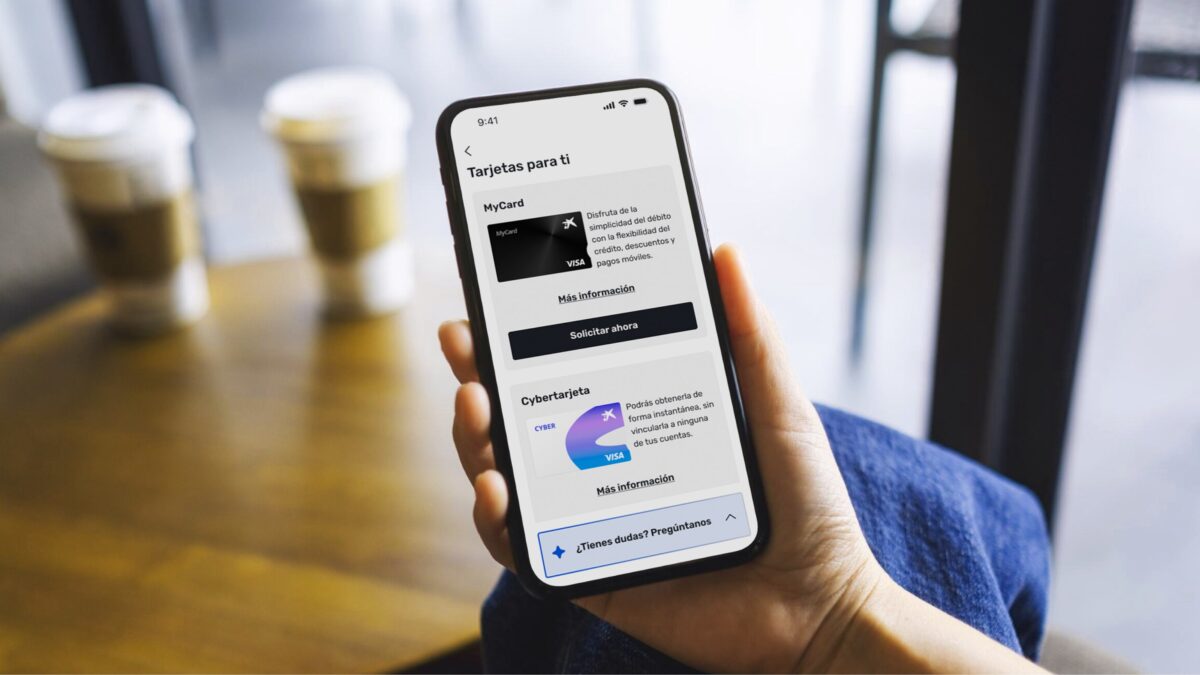

CaixaBank has rolled out an artificial intelligence agent aimed at accompanying customers who want to take out products within its app. The initiative aligns with the goal of turning the mobile phone into a primary sales and service channel, reducing friction in processes that often get stuck due to questions, comparisons, or a lack of clarity about terms and conditions.

According to information published by Finextra, the agent is designed to maintain a natural conversation with the user, with the aim of speeding up decision-making and improving the experience during digital onboarding.

In-app AI with human support

– What was announced: CaixaBank has deployed an AI agent to assist customers who buy/take out products within its app.

– How the “critical point” works: when it’s time to sign the contract, the agent hands off to a human specialist.

– Where it’s already in use: it is being used with customers who have started a pre-approved loan application in the app and run into difficulties, helping to define configuration, installments, and terms.

Sources: Finextra (“CaixaBank launches AI agent to help customers making in-app purchases”, 2026); CaixaBank (corporate note on its news website about the launch of the AI agent in the app, 2026).

Functions of the AI agent in the application

The new agent acts as a conversational assistant during the purchase, with a practical focus: helping the customer arrive at a specific product configuration and move forward without leaving the process.

Assistance in purchasing products

The agent accompanies the customer who is exploring or trying to take out a product in the app. In that conversation, it can provide additional information and guide them on options, so that the user better understands what they are taking out and which alternative fits their case.

The logic is similar to that of a “digital salesperson” within the application: it doesn’t just answer isolated questions, but sustains a dialogue to move toward completion.

Resolving queries and specifying needs

One of the core functions is helping the customer “pin down” what they need: what features they are looking for, what terms interest them, and what doubts prevent them from continuing. The agent answers queries and helps specify requirements, a critical point in financial products where indecision often arises due to details about installments, terms, or conditions.

From exploration to close

1) Explore: the customer enters the onboarding flow from the app and

state what they want (e.g., “I need a loan, but I don’t know what term suits me”).

2) Clarify and resolve doubts: the agent asks the minimum necessary to pin down needs and answers questions about conditions, options, and process steps.

3) Configure: the agent helps land on a configuration (amount/term/installment/terms) and understand the impact of changing each variable.

4) Confirm before closing (checkpoint): if the customer still has relevant doubts or it needs to be formalized, the flow prepares the handoff.

5) Refer to a human specialist: at the moment of signing the contract, the agent refers the customer to a specialist for closing.

Typical signs that the handoff is useful: repeated questions about final conditions, getting stuck on the last step, or the need for validation/security before signing.

Interaction between the AI agent and human specialists

CaixaBank’s model combines automation and human support at the most sensitive point in the process. When it’s time to formalize and sign the contract, the agent routes the customer to a human specialist.

This design aims to maintain the agility of digital self-service without removing personal guidance at closing, where final questions and the need for confirmation tend to concentrate.

| Part of the journey | AI agent (when it adds the most) | Human specialist (when it adds the most) | Value for the customer | Typical handoff point |

|---|---|---|---|---|

| Product exploration | When the user is comparing options and needs quick guidance within the app | When the case is atypical or requires a deeper, more personalized explanation | Less friction and more speed to understand alternatives | If the customer can’t decide after several clarifications |

| Resolving doubts | For frequently asked questions and immediate clarifications during the flow | For sensitive doubts or those that require contextualizing the customer’s situation | Answers in the moment, without leaving the process | When the doubt affects the final decision or trust |

| Configuration (amount/term/installment) | To iterate configurations and explain the effect of changes | To validate the final configuration and address objections | Greater clarity before committing | When the customer gets stuck or asks for final confirmation |

| Formalization and signing | Supportup to the previous step and prepare the handoff | At the contractual closing and signing | Trust and security at the decisive moment | “Time to sign the contract” |

Current use of the agent in loan applications

The agent is already operating in a specific use case: customers who have started a pre-approved loan application process and encounter difficulties along the journey.

In that context, the assistant helps define the “ideal configuration” of the loan, including elements such as installments, terms, and conditions, so that the user can complete the application with less friction and greater clarity.

Clarity in loan options

Practical example (pre-approved loan within the app):

– Situation: the customer starts the application, but gets stuck choosing between several combinations of term and installment.

– What the agent does: guides a conversation to pin down preferences (e.g., “I prioritize a low installment” vs. “I want to finish sooner”), and helps adjust variables such as term and installment to arrive at an understandable configuration.

– What is finalized: a configuration proposal with installments, terms, and conditions that the customer understands and can review.

– What it does not do at closing: when it’s time to formalize and sign, the flow is handed off to a human specialist.

This is the kind of friction point where a conversational assistant usually adds the most value: it does not replace the customer’s decision, but it reduces the cost of understanding options and moving forward.

Technology behind the AI agent

The initiative relies on third-party technology and on a roadmap for progressive expansion within the app, with the aim of scaling the conversational approach to more contracting processes.

Integration with Salesforce Agentforce

CaixaBank indicates that the technology is based on Agentforce, Salesforce’s offering for AI agents. This integration suggests an approach geared toward orchestrating conversations and service/sales flows within digital channels, with the ability to hand off to human teams when the process requires it.

Evolution toward recruitment chats

In the coming weeks, the institution expects the agent to evolve until it is integrated into the recruitment chats. The stated goal is to obtain information “efficiently, quickly, and flexibly,” extending the conversational pattern to more points in the digital funnel.

Key layers of the conversational journey

A simple framework to understand “what’s behind it” (without going into proprietary details):

– Conversational layer (front): the chat interface within the app where the customer asks, compares and

configure.

– Orchestration layer (Agentforce): coordinates the dialogue and the flow (what to ask, what step comes next, when to escalate), keeping the process within the contracting journey.

– Handoff layer: when it reaches signing or a sensitive point, it is routed to a human specialist for closing.

What to look at when assessing quality: consistency of answers with the conditions shown on screen, ability to maintain context (without “resetting” the conversation), and clarity of the handoff (that the customer understands why they are being transferred to a person and what will happen next).

Conclusions on the implementation of CaixaBank’s AI agent

CaixaBank’s bet illustrates a phase shift: from informational chatbots to agents that accompany purchase processes from start to finish, with handoff to humans at closing. If it works, it could redefine how financial products are sold on mobile: fewer screens, more conversation, and less drop-off.

Impact on the customer experience

The main expected impact is reduced friction: resolving questions in the moment, guiding the user when they don’t know what to choose, and preventing the process from being interrupted due to lack of understanding. Routing to specialists at signing aims to preserve trust and support in the final stretch.

Strategies for integrating AI in the banking sector

The “AI first, human at closing” approach is shaping up as a replicable strategy: automate product exploration and configuration, and reserve human intervention for validation, final personalization, and formalization. In addition, integration into the app places AI where conversion happens: the mobile channel.

Future challenges and opportunities in technology adoption

The immediate challenge will be scaling the agent to more products and conversations without degrading information quality or process coherence. The opportunity, on the other hand, is clear: turn the app into a more assisted contracting channel, with conversations that speed up decisions and allow human teams to focus on complex or higher-value cases.

Impact indicators in contracting

What to look at if you want to assess whether this type of agent “moves the needle” in digital contracting:

– Flow drop-off: whether it decreases at the steps where doubts used to concentrate (comparison/configuration).

– Conversation quality: whether the agent maintains context and responds in line with the conditions the customer sees in the app.

– Handoff clarity: whether the transfer to a human happens at the right moment (especially at signing) and without repeating information.

– Time to configuration: ifthe customer reaches an understandable configuration (installment/term/terms) sooner, without going in circles.

– Human team workload: if specialists receive better “prepared” cases (with needs already nailed down) and can focus on closing.

– Scaling to more products: if, when expanding to more contracting chats, consistency is maintained and the experience does not degrade.

Suricata Cx: Transforming the Customer Experience in Telecommunications

The Need for Innovation in the Telecom Sector

Telecoms face an environment of high competition, pressure on margins, and increasingly digital customers. Innovation in service and sales—especially in conversational channels—has become a differentiating factor to reduce operating costs and improve satisfaction.

How Suricata Cx Responds to Market Challenges

Suricata Cx proposes an approach focused on optimizing the customer experience through automation and intelligent assistance, with the aim of speeding up query resolution, improving service consistency, and sustaining demand peaks without degrading service.

Key Use Cases That Drive Efficiency

Among the common use cases in telecommunications are: first-level support, management of recurring incidents, order tracking, plan changes, and proactive retention. Conversational automation can reduce wait times and increase first-contact resolution.

The Importance of Human-AI Integration

As in banking, the value often lies in hybrid design: AI handles the repetitive and routes the complex. Integration with human agents makes it possible to maintain quality in sensitive situations (cancellations, complaints, critical incidents) and ensure service continuity.

Strategic Benefits for ISPs and Telecom Operators

A well-integrated model can translate into lower cost per interaction, greater service capacity, a better omnichannel experience, and more agility to launch campaigns or commercial changes. In a market where experience matters as much as price, operational efficiency and service quality become a competitive advantage.

Balance between AI and human service

Typical decisions when taking an “AI first, human at closing” model from banking to telecom (conversational CX):

– Scaling vs. consistency: automating more interactions increases capacity, but requires ensuring that information is consistent across channels (app, web, callcenter).

– Speed vs. trust: AI reduces waiting times, but in sensitive moments (leave, claim, critical incident) the customer usually values human confirmation.

– Operational savings vs. experience: lowering cost per contact works if it doesn’t increase repetition (i.e., the customer having to explain the same thing again when transferred to an agent).

– Self-service vs. real resolution: automating “the repetitive” adds value if the handoff is well designed and happens before the customer gets frustrated.

In practice, success tends to depend less on the “model” and more on two operational details: when escalation happens and what context is transferred to the human.

CaixaBank’s AI Agent for in-app purchases confirms that the conversational model “AI first, human at closure” is already maturing in sensitive processes such as contracting and signing. At Suricata Cx we closely follow this approach because it is exactly the kind of hybrid orchestration—combining automation with a controlled handoff to specialists—that makes it possible to scale the experience without losing trust or clarity at the decisive moment.

This analysis is produced from Suricata Cx’s perspective, focused on how hybrid models (AI + human supervision) are operationalized in real service and contracting flows in digital channels.

This text reflects publicly available information as of the publication date. Product details, use cases, and integration timelines may vary as the service evolves. For operational decisions, it is advisable to always validate actual behavior within the app.

Martin Weidemann is a specialist in digital transformation, telecommunications, and customer experience, with more than 20 years leading technology projects in fintech, ISPs, and digital services across Latin America and the U.S. He has been a founder and advisor to startups, works actively with internet operators and technology companies, and writes from practical experience, not theory. At Suricata he shares clear analysis, real cases, and field learnings on how to scale operations, improve support, and make better technology decisions.